October 31, 2022

Of the Series A terms you'll see in an agreement to sell preferred shares of your company to a VC, which terms are the most negotiated?

The term “Series A” refers to a sale of preferred stock by a company, usually to a VC firm. Series A typically follows significant progress by a company to develop its service or product and comes after earlier rounds of fundraising. A preferred stock term sheet consists of many industry standard terms, however, plenty of terms are negotiated heavily. While many of the terms mentioned below warrant a deeper dive, this post will provide a brief overview of the terms investors and founders most often negotiate in preferred stock transactions. Nothing in this post should be considered legal advice.

The National Venture Capital Association (NVCA) has developed a set of model forms typically used in preferred stock sales. The NVCA form set has been widely adopted by the startup industry and is increasing in popularity. Although the forms do not include an exhaustive collection of the possible provisions in preferred stock transactions, the NVCA’s aim is to reflect best practices and streamline most VC deals.

It is essential to be very thorough when negotiating the terms of the preferred stock transaction. As a founder, you want to understand how each of the terms affects your company’s operations, particularly your cap table, and you do not want to be surprised in the future by provisions that you overlooked during the preferred stock transaction.

Let's start by comparing some of the differences between common and preferred stock. Preferred stock typically offers its holders liquidation preferences, dividends, voting rights, and specific other rights not typically available for common stockholders. The common shares get their rights after the preferred stockholders are taken care of.

“Valuation” refers to the present value of your business. It is very likely the first term of negotiation in a preferred stock sale. We always recommend consulting a professional to help you determine your company's valuation before speaking to investors. Undervaluing your company can be significantly detrimental to your company's future fundraising.

Investors will want to negotiate your term sheet using either pre-money or post-money valuations so let's discuss the differences. “Pre-money valuation” refers to your company's value today, not including the investment. “Post-money valuation” refers to how much the company is worth after the investment. In the figure below, the ownership percentages will depend on whether the valuation is$1M pre or post-money. If the $1M is pre-money valuation, the post money ownership percentage of the investor will be 20%. If the $1M valuation is post-money, the investor ownership percentage is 25%. In the figure below, the valuation method used greatly affects the ownership.

When you determine the valuation of your company, you will need to calculate how all of the issued and outstanding equity will impact your cap table once the investment transaction is closed. This is called fully-diluted capitalization. The figure below shows that the fully-diluted capitalization includes the issued and outstanding common and preferred stock. Fully diluted consists of all issued stock, options, convertible notes, and other types of equity.

An important term is the amount of stock reserved for issuance under your company's equity incentive plan. This number is included in the fully-diluted capitalization. VCs will often require a certain percentage of shares to be reserved for issuance under the equity incentive plan (EIP) after the investment. It is important to understand whether the percentage of shares reserved for the EIP is calculated pre-money or post-money.

One item to note is that dividends are often negotiated on preferred stock term sheets. Rights to dividends can be given to the preferred share investor, although your company's board of directors determines if and when the company will pay dividends.

The term “pari passu” may not expressly appear in your term sheets, however, it is crucial to understand what it means when it comes to future rounds of preferred stock. Most preferred stock transactions will include a provision where each series of preferred stock will be treated equally with respect to dividends, distributions, or proceeds in a liquidation event of your company.

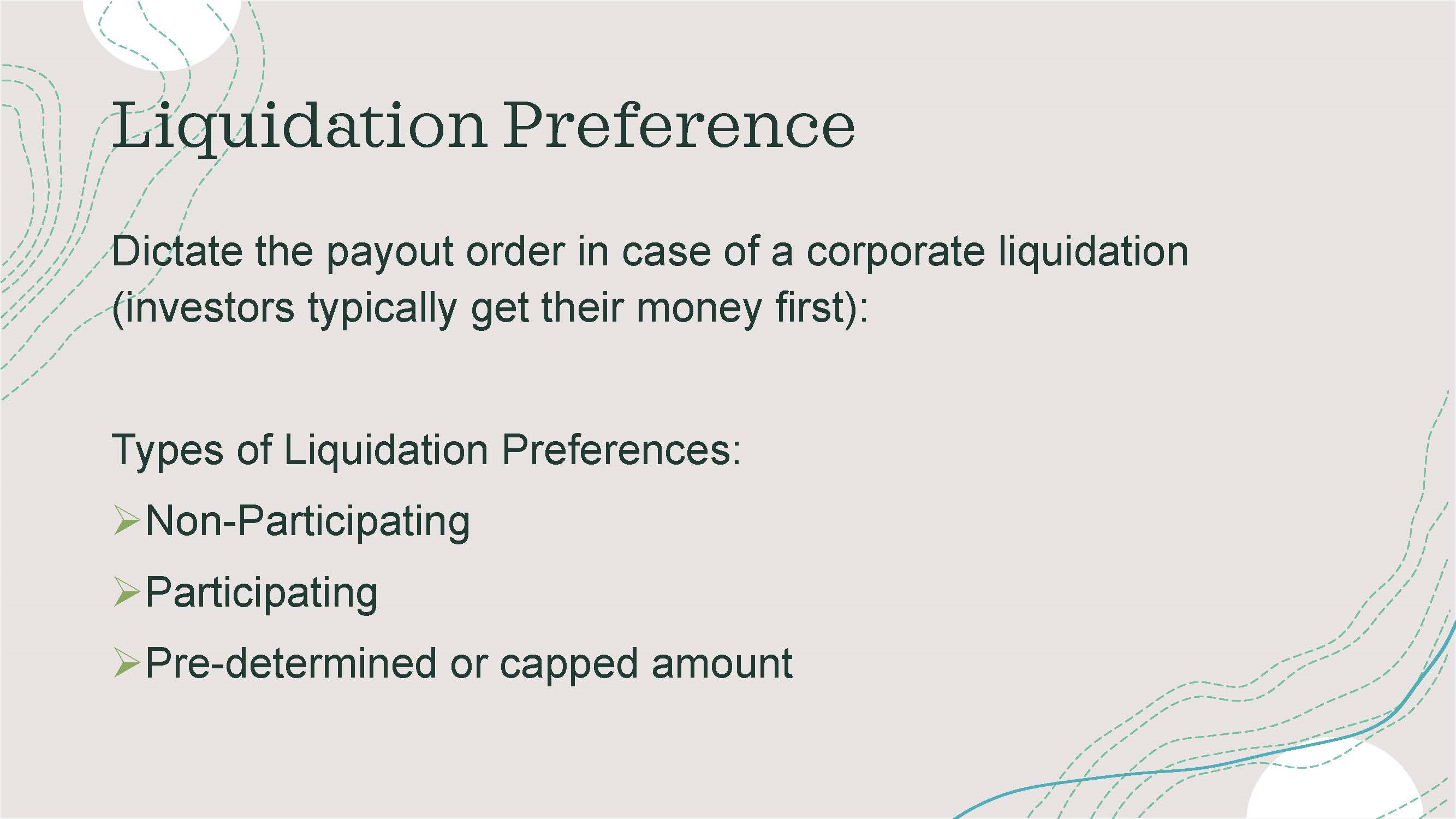

The liquidation preference prescribes the order in which your stockholders receive funds in the event of a liquidation of your company. It gets technical, but the below graphic lists different types of liquidation preferences that you need to be aware of before signing your term sheet.

The most desirable liquidation preference on the startup side is non-participating preferred. In this scenario, the investor's distribution is limited to the amount of its liquidation preference. One times their investment amount, two times the investment amount, and so on. Less desirable is participating preferred, which is when, after the investor receives its liquidation preference, it participates with common stockholders in the remaining amount of funds available for distributions. This preference brings the investor a much higher return on their investment and reduces the amount left over for the common stockholders.

Preferred stock investors typically receive certain voting rights with the purchase of their preferred stock, allowing them to represent their specific stock on some issues brought before the stockholders. These items include, but are not limited to, selecting a member to serve on the board of directors of your company and approving the increase in the number of authorized shares of stock your company can issue.

The figure below lists some items that may be included in the term sheet that require the approval of your preferred stockholders. These rights are protective provisions. Your preferred stockholders want to protect their investment by voting on certain transactions of your company.

Another common term concerns conversion. Conversion is when the preferred stock converts to common stock, usually at your investor’s option or upon the company going public. Conversion typically happens on a one-for-one basis or one dollar for one dollar. For every dollar of preferred stock, the investor will receive one dollar of common stock when converted. Conversion maybe optional to your preferred stockholders.

A phrase that will appear in several places throughout your term sheet is the phrase on an “as-converted” basis. The as-converted basis determines the number of shares in the preferred class necessary to approve an action of the stockholders. If we are using the one dollar for one dollar conversion ratio, your preferred shares generally result in a higher number of votes because the preferred stock has a higher dollar value than common stock, so be sure you calculate the "as converted" number when determining the number of votes necessary to approve certain transactions that require the preferred stockholders' vote. This calculation is often overlooked in voting matters. It makes a more significant difference when there is more than one type of preferred stock issued and outstanding.

Anti-dilution protects your preferred investors against any down-round stock sales. Suppose your company decides to sell securities at a price lower than the price sold to your current preferred stockholders. In that case, an anti-dilution calculation will be used to determine the number of additional shares of stock your current preferred investors will receive. Hence, they keep their ownership position in your company. A broad-based anti-dilution provision is most common in preferred deals. The calculation will include your fully-diluted capitalization numbers when determining the number of additional shares your investors receive.

Pay-to-play incentivizes investors to participate in future rounds of financing. Simplistically, investors that do not participate to their full pro-rata percentage of the next financing round lose the right to pay-to-play in the future.

Some preferred stock investors may require that the company buy back their shares of preferred stock. Redemption can happen after a certain number of years and over a certain period of time.

The preferred stock purchase agreement will contain representations and warranties covering factual statements about your company. It is essential to disclose this information because an omission of information that should appear in this section may result in future problems. Common areas for reps and warranties are listed in the figure below.

Your preferred investor may require your company to pay for a certain amount of their legal costs and expenses related to purchasing the preferred stock. This expense is over and above your own legal fees and costs.

Registration rights for preferred stockholders typically occur a specific number of years after closing the preferred stock transaction or shortly after your company's initial public offering. The set of registration rights listed in the figure below is typical for preferred stock term sheets.

The lock-up period is a holding period during which stockholders cannot sell their stock. Lock-up happens upon filing an initial public offering and prevents stockholders from selling their shares too quickly, which shows that the company leadership remains intact. Lock-up periods typically last for 180 days after an IPO.

Management and information rights are granted to only certain of your preferred stockholders, referred to as major investors. The major investors remain informed of a specific list of information related to the company. This information may include quarterly financials, budget reports, and updated cap tables detailing transactions that may affect their equity position. Your major investors may be entitled to more information over your other preferred stockholders. In some circumstances, the major investors possess voting control of that particular series of preferred stock.

Pro-rata rights are often granted to your preferred stockholders, allowing them to purchase up to their percentage equity ownership in the subsequent financing rounds. Sometimes this right is limited to only major investors.

If your preferred stockholders are granted the right to elect a director, certain actions, as shown below, require the affirmative vote of that preferred director to be approved by the board of directors.

Your documentation must include non-disclosure and non-solicitation agreements. Investor counsel will want to review these documents during the due diligence phase of your transaction. It is also essential to have your non-compete agreements in order before you sign your term sheet. Having proper documentation for your company will cut down on time needed for due diligence.

The preferred stock investors will likely require that future grants of options to purchase common stock be granted with standardized vesting requirements. Option vesting may include a cliff, or period of time before vesting begins, and will likely last several years before all of the options have vested.

Rights of first refusal are common in a preferred term sheet. Such rights are triggered when certain stockholders wish to sell or transfer their shares. Your preferred investors would have the option to purchase the shares instead. This right also ensures that preferred stockholders know who is receiving shares in the company.

Along with the right of first refusal usually comes the co-sale right, or tag-along right, which allows your minority stockholders to participate in a sale if majority stockholders sell their shares. Co-sale rights are beneficial to minority stockholders because a majority stockholder can usually negotiate better terms for selling their shares than a minority holder. The majority stockholders may also have the right drag along the minority stockholders to join in a transaction in which more than 50% of the company's voting power is transferred.

It is not unusual for your investor to request that, for a certain period of time, you do not shop for a better deal.

If you've made it this far, you have noticed that the rights and preferences for preferred stockholders are vast, and this post, by no means, captures every issue that may come up for discussion during term sheet negotiations. Some provisions can be very complicated, so don't sign a term sheet before consulting with counsel and understanding what each term represents to your company.

For more information about Series A deals or preferred stock sales, please contact us at info@afissio.com.